Design to Target Cost (DTC) Methodology

Overview of Design to Target Cost

The definition of Design to Target Cost is “The process of monitoring and controlling the future manufacturing cost of a product during the Product Introduction Process.”

It is market driven costing system in which cost targets are set by considering customer requirements and competitive offerings. Cost targets are achieved

or attained by focusing on product and process design and by making continuous improvements in all support processes.

The Design to Target Cost methodology aims to:-

- Set and verify a target manufacturing cost for a product in a competing environment where this cost is based on the selling price expected and the profit required.

- Systematically identify the sub-system cost targets within the product.

- Evaluate the commercial feasibility of the design, manufacturing and distribution concepts during the conceptual stage.

- Construct a product cost model.

- Do the necessary detailed product and process design to attain the target cost.

- Update the cost model constantly during the Product Development Process.

- Identify any potential cost drifts and take action to bring the costs back onto the target.

There is one clear fundamental rule in Design to Target Cost.

Achieve the target cost and the product has the potential to make profit - miss the target cost and the product will loose money!

Design to Cost Methodology Overview Diagram

1.0 - Set Target Costs

1.1 - Assessment of Market Selling Price

Selling price is the subject of many books and theories that suggest how to work out what it should be. A simplistic way of defining a market price for a product is that it equals the value to the customer of that product or service where there may be competing products.

The customer will have a different view of the value of a product depending on where he is in the supply chain. The seller may also have strategic or tactical reasons for setting a price at a certain level.

Considerations in setting or identifying a products market price include.

- Manufacturing and Supply Costs

- Demand

- Competition/Market Structure

Target Cost and Customer Demand

The Design to Cost method sets a manufacturing cost target based on market price and profit requirements. Care is needed in that in some markets customers will have a clear view of the cost of manufacture and may not place the profit requirements as high as is needed. In other target markets a low price may indicate to customers something inferior about the product. In this case the profit margin may need to be set higher to provide a valid target cost that allows for downward price movement should competitors enter the market with similar products.

Two interrelated questions need to be answered:

- What will be the likely quantity demanded at any given price?

- What will be the effect on sales volume of changes in selling price?

A simple demand curve, such as diagram 2, contains important information which will allow a company to ascertain the relationship between the price charged and the resulting level of demand.

Care, however, is needed. Industries which are earlier in the supply chain may find that once a customer has made the decision to source their sub-system, price has no effect on quantity. Indeed it may be the other way round: quantity affects the cost.

For example in the automotive industry where there are no guarantees from the vehicle manufacturer to component suppliers on the probability of achieving a particular demand level, the component supplier may wish to negotiate a price which is related to demand levels.

Such a contract has implications for Design to Target Cost, because the target cost may also follow a curve based on quantity.

Competition/Market Structure

Companies in differing product markets find themselves faced with varying degrees of competition. Some markets are characterised by large numbers of competitors, whereas others may comprise of relatively few companies competing for the same customers.

- Where the number of competitors selling similar or identical products, competition on price will be severe.

- Where there is only one supplier, he may establish his own price, within the constraints of government legislation.

Clearly most markets fall between these two extremes. The overall aim of product development should be to drive towards solutions at both ends of the market.

- On the one hand the aim is to reduce the manufacturing cost through effective design and efficient manufacturing methods. i.e. minimum parts count servicing maximum product variety though modular design concepts, appropriate materials and process technology and streamlined manufacturing methods.

- Whilst on the other hand differentiating your product from others so that the customer's decision is less based on price.

The product introduction team should include marketing specialists who are familiar with the decision making logic of customers.

First stage Quality Function Deployment (QFD) should be used to understand the customer requirements, including the price.

The approach to setting market price will differ depending on the situation.

a) One Customer - bespoke, variant or custom design.

Typically in the manufacturing supply industry a customer will approach known suppliers of components and sub-systems and ask them to prepare a tender. The customer will usually prepare a technical specification for the sub-system which will be subject to some change after award of the contract.

The aim of the supplier is to set a price, or a range of prices set against volume, which will ensure that the contract is won. In some cases there will be the possibility to alter the price should the customer change his original requirements. We need to be clear that price will not be the only criteria for contract award.

QFD should be used by the team to quantify all the customer's requirements, including price. The team should also use QFD to identify the competition and their pricing strategy.

b) Many Potential Customers - product families, a standard product range, or standard product.

Companies who supply one product or a range of standard products to a large number of customers perhaps through numerous distribution agents need a differing approach to setting the market price.

They need to understand the price demand curve both for the industry sector they are in and their company within that sector. They will need to understand their distributor’s requirements for profit and mark-up they in turn require.

Again QFD1 should be used but the team should be aware that the selling price they are identifying needs to be in terms of both the distributor and the end customer.

1.2 - Setting Target Cost

Having identified a selling price for the product the deign team needs to use this information to set the target cost. Simplistically it is possible to state that:

Target Cost = Selling Price - Profit Requirement

The profit requirement can be defined as a number of financial goals which state the minimum required for the company's shareholders to receive an adequate dividend and growth from investing in the company. This would define the maximum target cost. The executive of a company must communicate the true needs for profit, return on investment, return of sales etc. to the Product Introduction team. They should take into account industry norms and assess the gap between where they currently are placed against the best in class.

The Product Introduction team should also make comparisons against any current similar products which they make, to crudely evaluate the feasibility of achieving the target cost - perhaps using parametric or comparative cost estimating methods at this stage.

Identification of Sub-System Target Costs

The more complex the product the more sub-systems there are likely to be. The total product cost is simply the addition of each sub-system cost plus the final assembly cost.

The Design to Target Cost Methodology manages the cost of each sub-system where there may be separate design teams and suppliers responsible for each sub-system.

Design to Cost gives the responsibility for cost to the teams which means they need to understand this very clear point:-

If every sub-system is supplied at or below its target cost then the total product cost target will be achieved and the product will have the potential to be a commercial success. However, if any one of the sub-systems does not achieve its target cost then the whole product will be a commercial failure.

Put another way - each design team must believe that if they fail everyone fails!

1.3 - Create or Define Product Structure

The design team must create an accurate hierarchical product structure or Bill of Materials (BOM). Each sub-assembly must be documented without abiguity.

For example, do the seats include the cost of the mounting method or is that part of body in white?

A Typical Hierarchical Product Structure

1.4 - Identify Sub-System Costs

Classify Sub-Systems

- Identify sub-systems which already exist and a cost known e.g. using an existing engine design.

- Identify sub-systems which are similar to those that already exist and a cost known. e.g. suspension where the differences are geometry, spring and damper rates and bush compliance.

- Identify sub-systems where something exists with the same function although the way it works is different. e.g. A carburettor and fuel injection system both mix fuel and air as their basic function.

- Identify sub-systems where similar technologies are used in other industries to carry out a different function.

- Identify sub-systems which are entirely new to your company.

In practise it is expected that about 85% of sub-systems fall into the first 3 classifications.

Estimate Sub-System Costs

The Product Introduction Team will include estimating specialists from the business but the setting of the cost targets should be a team activity.

The following rules must be followed:

- We are interested in a true cost. We define the sub-system cost as an "In Place Cost". That is: All the costs associated with managing the purchase, and storage of raw materials, carrying out the processing and includes the assembly cost to fix the sub-system to the whole product. This implies that Activity Based Costing is used as best practise. However, if Activity Based Costing has yet to be implemented, the design team should not be prevented from using other costing systems, provided that common sense is used.

- Where we are using a known cost we need to bear in mind the effect of volume (demand) on the cost where perhaps a lower cost would result. The cost model should be set up to handle price breaks for components automatically. So when the model volume changes the actual prices for whole systems and subsystems change automatically. This will save huge amounts of time should the product volume assumptions change.

- We also need to bear in mind the cost associated with managing product variety. i.e. if there is a stated intention to fit higher specification/or performance variants to the top of the product range - has the effect on cost been examined closely, due to reduced volumes and increased variety management, at the lower end of the product range? For instance, would it cost less to fit all cars in a model range with power steering rather than have both manual steering and power steering varieties produced?

- It is okay to use guestimates, parametrics, and supplier estimates. It is okay to use difference evaluation, but outright, full blown detailed cost estimated at this stage should be reserved for unknown sub-systems where confidence is low and risk high.

- Manufacturing Analysis is a good way of carrying out quick estimates of cost and can be applied to the whole sub-system or just the known functional differences.

1.5 - Verify Cost Targets

Having made the estimates on cost the team will fit them back to the product structure to note any variance. What usually happens is that the sum of the sub-systems will add up to more than the target cost.

The team need to close the gap. Questions they might answer include:

- Are there any functions which have no real value to the customer?

- Are there any sub-systems which we believe could be reduced in cost?

- Are there any sub-systems which have a higher value to the customer than the cost estimate implies?

- Are there any sub-systems where we could use an existing design, thereby reducing development costs?

- Are there any sub-systems where we could take a standard product from the supplier?

- Are there any areas where there is unnecessary variety?

Note: In automotive companies world-wide there is a stated aim generally that suppliers will need to reduce cost by 20% as soon as possible. If there is still a gap, maybe the team need to set challenging targets, which are achievable with focused effort.

The sub-system target costs should now be fixed.

2.0 - Attaining Target Cost

2.1 - Using the Product Cost Model

The team need to understand the way the cost model is likely to be used.

Initially the cost model will be a product cost estimate based on a product structure where detailed information about the product is both vague and fluid. If a PLM system is being used to manage the prototype Bill of Materials (BOM) then data controls should be set that are appropriate for the concept design phases.

It would be folly to impose production phase data management and engineering controls at this early stage. At this stage the cost model is based on many assumptions which Product Introduction teams must turn into a practical reality and that cannot be done at speed with unnecessarily restrictive data change controls.

As details become firmer about the product configuration and so the team will be able to obtain more detail which will become more accurate. As the design becomes progressively embodied as CAD models with a verified technical performance and cost established then tighter data controls can be applied the closer the project gets to the launch date.

Diagram 4. Cost Model Confidence Graph

Diagram 4 shows a likely confidence level in a cost model for a typical sub-system with a high degree of newness. It assumes that the basic design concept does NOT undergo significant change.

Clearly the biggest step in confidence with cost will occur from the information generated during the conceptual design phase.

The team should be encouraged to analyse the cost of manufacture using Manufacturing Analysis and Design for Assembly (DFA) tools. When using component Manufacturing Analysis or parametric costing they should direct it at those components which are likely to have the highest costs. They should also take into account their own confidence concerning likely costs.

Following concept design, the detailed design phase, will allow the team to begin defining the manufacturing methods. The team can use product costing systems that derive cost direct from the CAD models – if they exist at this stage. It will also allow the team to obtain detailed confirmation quotations from suppliers.

The proven approach is:

With every change, receipt or generation of new information, firming of details, and quotations etc. the cost model should be updated. e.g. Having given the supplier of the fuel injection system new information about positioning and type of fuel and electrical connections and revised the position and space envelope of the control module, he is able to turn a ball park price estimate into a firm quotation. New information is immediately added to the cost information on the product structure so the next cost roll-up will take it into account and everybody will be informed of its effect.

Diagram 5 shows a typical cost model.

At the top level the team will list the main sub-systems and their target costs. This is the Product summary. They will also list the latest cost estimate of the sub-system and the variance. Some systems use traffic lights to highlight how close to target the drifting costs are.

Diagram 5 – Spreadsheet based Design to Cost System

This latest cost estimate could come from various sources.

Initially it could be based on a parametric estimate or some comparison. This could mean that during the concept phase the only level available is the systems level.

The next level will be a sub-system summary chart. The design team should list all the parts, the number required, the target cost, and the latest estimate for that part in that system or subsystem.

Whilst not essential, the design team will benefit from setting targets for all new components defined during concept design. Component targets may be set in a similar way as previously. In this way the team can check component targets add up to the sub-system targets. The estimated cost for each part will come from one of 6 sources (although there may be more).

- Parametric Estimates

- Manufacturing Analysis

- Product Cost estimates derived from the CAD model.

- Detailed Production Planned Cost Estimate

- Knowledge currently available.

- Suppliers Quotation (suitably verified against known costs)

2.2 - Assumption Action List

At all stages of product introduction cost estimates at all levels of the product cost structure will be based on many assumptions.

These assumptions take many forms, including:-

- Assumptions about tolerance, surface finish and material specification,

- Assumptions about the price suppliers will charge, and

- Assumptions about the achievable manufacturing times.

During early stages of concept design these assumptions may even be about the final product structure. The rule for the team to remember is:

Every estimate about cost is based on an assumption which must be turned into reality during product introduction.similar to an FMEA action list. Diagram 5 includes a typical assumption action list. The team should review it regularly and measure their performance against it. If using PLM the Workflow module could be used to monitor the action list and route work to the designated persons for action.

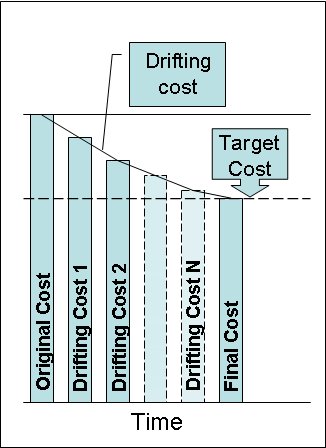

2.3 - Drifting Cost or Cost Variance and Team Action

The Design to Target Cost methodology is there to identify and expose the cost drift to the design team and management. It also ensures cost does not creep out of control.

As the cost model is updated with the latest new information, throughout the products introduction, so cost drift will occur. Primarily this will show up as a sub-system variance, when the estimated cost of the sub-system exceeds its target cost.

Therefore all product design decisions must be made in conjunction with viewing the impact on the product cost. The key benefit of having this real-time indication of a drifting cost problem is so that design action can be taken before it is too late. A good question is, "What action should be taken?"

Clearly this depends on many factors. Some of the factors will be conflicting and have to be balanced to meet the profit / market introduction / customer requirement window:-

- Should new component suppliers be sought?

- Should we put pressure on existing suppliers?

- Should we go back to our basic assumptions about the product performance requirements?

- Have we truly considered all the materials and process alternatives?

- Should we leave out certain costly functions?

- Are we using custom parts or could we use something off the shelf?

- Have we really done our Value Analysis or Value Engineering thoroughly?

- Will the proposed actions still allow job one to be delivered on time?

The product team needs to decide on the best course of action in their particular business circumstances.

Actions which can only be taken with very senior authority include:

- Changing the Target Cost, (Widening the Goal Posts),

- Altering the sub-system cost allocation break down (Robbing Peter to pay Paul), and

- Missing product launch date or Job One (Late to Bed Late to Market).

In periods of intense team activity, such as during a DFA exercise, where the product concept may change considerably in a very short space of time, it may only be practical to update the cost model at the end of the exercise to take into account all the proposed changes.

Conversely, at other times during Product Development every new scrap of information needs to be input as soon as possible.

2.4 - Bought in Sub-Systems and Components

The purchasing - supplier interface needs to understand that if a supplier achieves the cost target purely by cutting his profit, his long term survival is jeopardised. Instead the purchasing functions need to make sure the price is achieved by the supplier cutting the sub-systems manufacturing cost using Design to Target Cost methods.

Supplier development is therefore required for key suppliers. Help the supplier because the cost of losing good suppliers can be very high indeed. In the ideal Design to Target Cost environment key suppliers will be operating with an 'open book' policy. Because of the strategic nature of these suppliers it is essential that they remain at the forefront of their particular expertise and they remain viable in the long-term.

However they need to offer competitive prices which meet the target cost for their particular sub-system.

Supplier Development/Purchasing functions need to be involved in Product Introduction and apply Design to Target Cost rules to the supplier. Supplier team action where cost drift occurs should mirror that in their customer’s organisation.

3.0 - Production Ramp-up and Handover

The Design to Target Cost methodology requires that the product introduction team own the cost model until the product is handed over to manufacturing for production. Handover takes place when there is agreement of 'Demonstrated Capability'. That is, when the manufacturing cost is fully proven on the shop floor. In exceptional circumstances, however, if a sub-system fails to meet its target, cost plans should be put in place to work towards its eventual achievement.